Uncharted Waters

It is now apparent to just about everyone that someone other than Joe Biden or Donald Trump could win the November election.

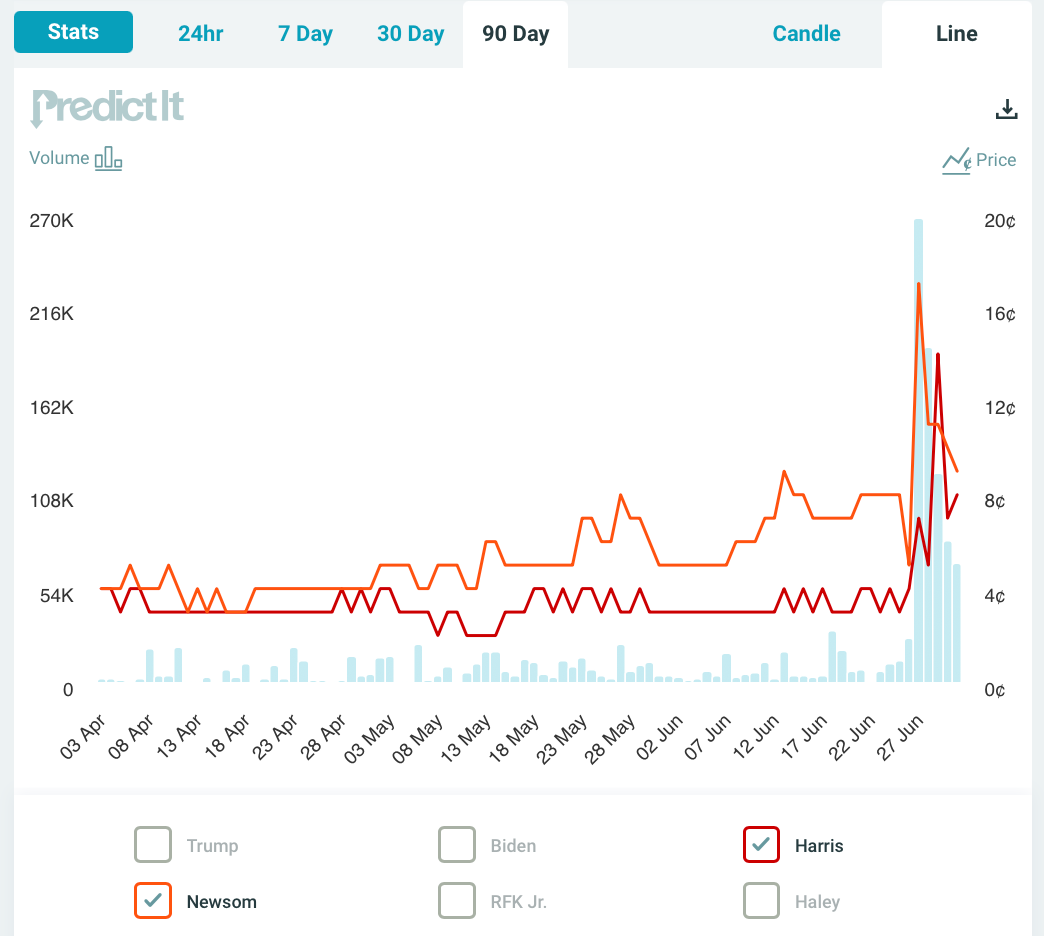

This realization has taken many by surprise, but traders on prediction markets have contemplated the possibility for several months now. Here, for instance, are the prices of contracts referencing Harris and Newsom in the presidential winner market over the past ninety days:

Prices rose sharply amid heavy trading volume during and after the debate, but were not negligible prior to that, with the likelihood that one of these two would be elected president reaching double digits at times.1

Meanwhile, several statistical models constructed to predict the election winner are still assigning essentially zero probability to any outcome in which the winner is not named Trump or Biden. The Economist model splits 73-27 in favor of Trump:

Nate Silver’s model is in the same ballpark:

And the FiveThirtyEight model sees the race as a toss-up:

All three predictions have been updated since the debate. If Biden steps aside or is replaced, these models will have to be substantially modified and will lose continuity. They have already lost reliability.

As discussed in my last post, statistical models perform well only when the past is a reasonably good guide to the future. Models are built and calibrated based on historical data, under the assumption that the data generating process has not shifted dramatically. They run into real trouble when we enter uncharted waters.

Highly consequential decisions are being made by political elites as we speak, and these choices hinge on beliefs about the strength of various potential Democratic candidates in November. Opinion polls can offer some guidance here but very little, since they cannot account for strengths and vulnerabilities that will emerge only after campaigns are officially launched and candidates are subjected to media scrutiny and opposition research.

So all we have as a guide for the moment are markets. These can be used to estimate conditional probabilities—the likelihood that a candidate will win the election conditional on being the nominee. As a rough approximation, this can be done by dividing a candidate’s price in the presidential winner market by that in the party nominee market, though some scaling is required to make sure that these correspond to probabilities.

But even here we have a problem, because of the potential for manipulation. For example, supporters of a candidate can trade in ways that lower the implied likelihood of nomination while raising the likelihood of eventual victory. And those who would like the party to lose can boost the weakest candidate in this way.

Is manipulation common in prediction markets? A few years ago David Rothschild and I were examining transaction-level data from Intrade and discovered an (anonymized) account that had bet seven million dollars on Mitt Romney in over twenty thousand separate transactions over a two year period leading up to the 2012 election. One cannot rule out pecuniary motives but the pattern of trade was suggestive of an attempt to place a lower bound on the price of the Romney contract, possibly to prevent a collapse in morale, donor support, volunteer effort, and other ingredients important to a campaign.2

While incentives for manipulation exist, and attempts are not uncommon, they are only marginally successful for short periods of time before others see a profit opportunity and pounce.

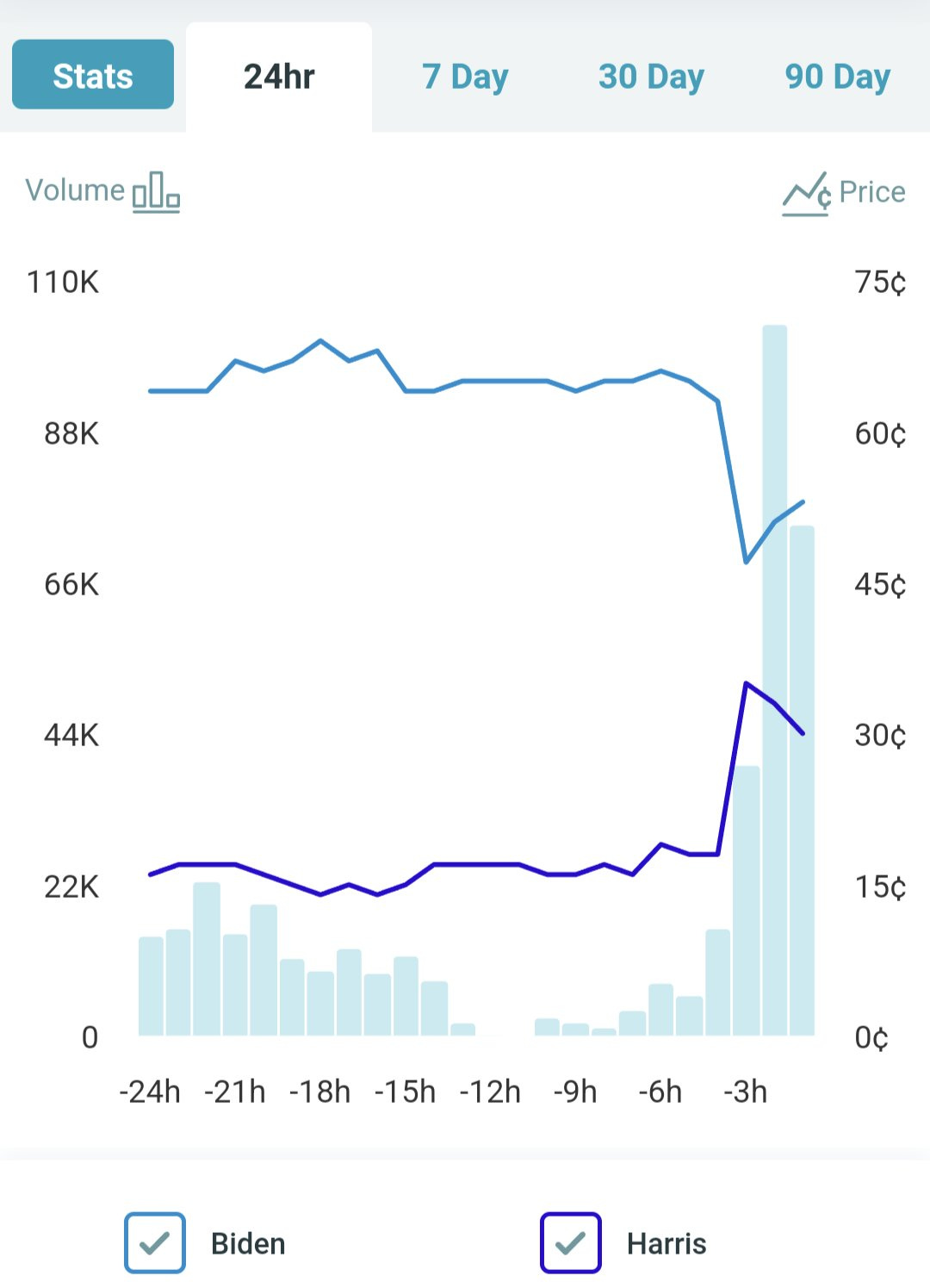

Even setting aside the possibility of attempted manipulation, prediction market prices offer a very imperfect signal of electoral viability at the moment, especially with news coming in thick and fast and prices extremely volatile. In just the past couple of hours, there have been large movements in the market for the Democratic nomination:

These prices can’t last for long, one or both contracts will collapse towards zero as uncertainty is resolved.

Where does this leave us? Decisions that will have an enormous impact on the direction of the country will be made largely on instinct, as we collectively fumble in the dark. Once the dust settles, so will markets, and we will start to see more signal and less noise.

For a relatively informal introduction to the structure and functioning of peer-to-peer prediction markets, see my conversation with Sean Brady on the Simplifying Complexity podcast. For a more technical presentation that includes some recent research findings, see this recording, posted just a couple of weeks ago in preparation for a Santa Fe Institute summer school to be held in Bogotá later this month.

Our goal in the paper was to map out an ecology of trading strategies, in hopes of learning something about how information is absorbed by financial markets quite generally. Media attention, understandably, focused entirely on this one large trader (see, for example, the reports in CNBC, WSJ, Politico, Atlantic, and Slate).

"Meanwhile, several statistical models constructed to predict the election winner are still assigning essentially zero probability to any outcome in which the winner is not named Trump or Biden."

I get the concern and agree that historic indicators may end up failing to be as useful in this race, but I still think these models provide some important qualitative information. Conditional on the election coming down to Biden-Trump, Biden is on shaky footing, particularly for an incumbent. Everyone in the social media pissing matches about Biden's chances are lobbing single polls (with lots of variance). No one considers that pretty much all the models, regardless of their result probabilities, started to show the same trend *before* the debate: Biden's chances at winning the Electoral College were falling, precipitously. I doubt that's all noise, even if the probabilities themselves shouldn't be interpreted literally.

Coupled with the signals in the prediction market, I think that all points to Democrats needing to consider seriously whether they can find someone who 1) can beat a coin flip and 2) will reduce the uncertainty somewhat, though #2 may be wishful thinking at this point.

(In the past couple elections, I think the Economist's poll outperformed the 538 models further out, even though they ended up in similar places by the day of the election. I don't have a good feel for how 538's new forecasting approach has changed post Silver's exit.)

On the point of the Intrade bettor who had a $7 Million on Romney, is it possible he was arbitraging with prices on a secondary website? This kind of thing is common in sports betting