Information Contagion

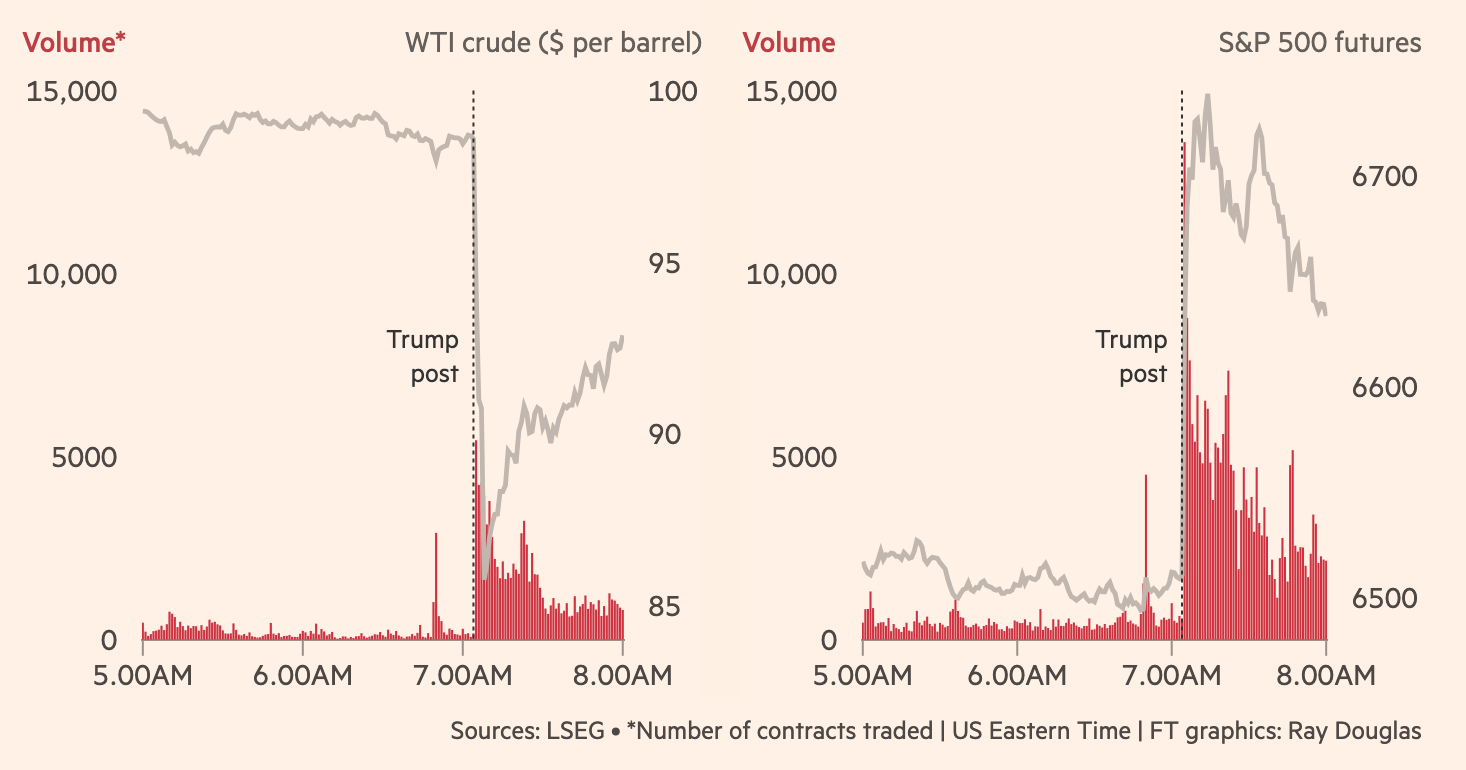

At around 6:50am ET on March 24, there was an unusually large spike in trading volume in oil and stock futures markets. Fifteen minutes later, Donald Trump announced on social media that productive negotiations with Iranian officials were underway, and that he would not be acting on his threat to bomb power plants for at least another five days.

The post had an immediate effect on asset prices, with oil falling sharply and stock indexes surging. The following graphic from the Financial Times shows both the effects of the announcement and the burst of trading activity that preceded it.

Whoever entered large short positions in oil and long positions in the stock index made millions in minutes.1 This naturally led to speculation that this was a political insider profiting from proximity to the president. Paul Krugman, among others, was convinced that “somebody close to Trump knew what he was about to do, and exploited that inside information to make huge, instant profits.”

This episode resembles startlingly well-timed trades prior to the capture of Nicolás Maduro and the initiation of military strikes against Iran, with one very important difference—the earlier activity was on crypto-based Polymarket where most trader identities are not known even to the platform, while these recent transactions were on regulated exchanges required to abide by know-your-customer (KYC) laws.2 That is, if federal officials or regulators choose to do so, they can demand information on the individual or entity who placed these orders.

Why would someone with inside information about national security decisions risk exposure by placing such large orders in regulated financial markets? It’s possible that they did so via an offshore shell company, which would make the original source difficult to trace. But this would require a very different set of competences than the kinds of well-timed trades we have previously seen, which have used anonymous crypto wallets on Polymarket.

There’s another possibility worth considering.

The trades in oil and stock futures may not have come from an insider at all, but from a quant fund that extracted the inside information from prior trades on Polymarket. For example, on the weekend of March 22-23, a number of wallets placed bets on a ceasefire by the end of the month in a manner that looked to be coordinated, and led to a sharp but temporary price increase. One of these wallets had previously made significant profits on the timing of the initial strike. These accounts are likely to lose money on the ceasefire bets, but their activity may have signaled to others that negotiations were underway.

The point is this—if insiders believe that they can trade without fear of detection on Polymarket, then more conventional investment vehicles operating on a larger scale will be on the lookout for signals of insider activity. They can extract and exploit information coming from insiders without themselves facing legal jeopardy. Information bleeds across venues, with insider trading on one exchange leading to insider-like trading elsewhere.

One reason why American securities laws prohibit insider trading on regulated exchanges is that it discourages outsiders from participating, resulting in lower liquidity and wider bid-ask spreads. Liquidity providers who post orders on both sides of the market are especially vulnerable to being picked off.3 What the events of last Monday reveal is that the absence of know-your-customer regulations on one exchange don’t just affect traders at that venue. Like information itself, the absence of regulation is contagious.

The market reaction to a second deadline extension a few days later was more muted.

According to a CNN report, federal prosecutors are looking into unlawful insider trading on Polymarket. Since all transactions are on a public blockchain and the exchange itself doesn’t know who owns the implicated wallets, it seems to me that investigators will need to engage in blockchain forensics or outsource this to specialized firms if they want to identify insiders.

For a formal analysis of the adverse selection problem faced by market makers, see the classic papers by Glosten and Milgrom and Kyle.

The regulatory arbitrage here is even more structurally entrenched than it appears. The CFTC oversees Polymarket (nominally), the SEC handles equities, and the CFTC separately regulates oil futures — three agencies with no unified cross-market surveillance framework. When the SEC brought its 2015 case against Barclays' dark pool, the core issue was information leakage to HFT firms *within a single regulatory regime*, and even that took years to prosecute. What you're describing is information laundering across regimes: signal enters through an unregulated crypto venue, gets cleaned by appearing as observable price movement (which is perfectly legal to trade on), and exits through regulated futures markets. The quant fund in your scenario isn't breaking any law — they're reading a public price feed. The insider is the only one exposed, and only on the platform least equipped to identify them.

Great article and very interesting take!