The Venezuela Windfall

Major economic, political, and military decisions move asset prices, and those with foreknowledge of such things can make significant trading profits. For example, the placement and easing of tariff protections had a predictable whipsaw effect on the stock market, and even statements hinting at such policy shifts can result in large asset revaluations.

But using stocks (or other conventional securities) to profit from inside information faces two challenges. First, trading cannot be done anonymously, since regulated financial institutions face know-your-customer (KYC) requirements. And second, stocks are affected by a broad range of factors, and so trading on foreknowledge of just one of these carries some degree of financial risk.

For those seeking to profit from proximity to power, the proliferation and growth of prediction markets has solved the latter problem. One can now buy contracts that reference exact events—ranging from the elimination of federal agencies to the seizure of the Panama Canal. And the presence in this space of markets that use stablecoins as the medium of exchange addresses the former challenge, allowing traders to conceal their true identities.

The fact that anonymous trading on inside information has become easier and more profitable means that more people are on the lookout for suspicious trades. One recent case involves an account that first traded less than two weeks ago, placed seven well-timed bets on the ouster of Nicolás Maduro at a cost of $32,537, and ended up with a quick profit of $404,222. These trades aroused interest even before event realization, and have been covered by several media sources since.

It has been reported that some news organizations had advance warning of the raid, so it’s possible that the information leakage originated there. But the first trade was on December 31 at 12:20am UTC, days before the seizure was made public at 9:21am UTC on January 3 (4:21am on the East Coast). So a leak originating with the media seems unlikely to me.

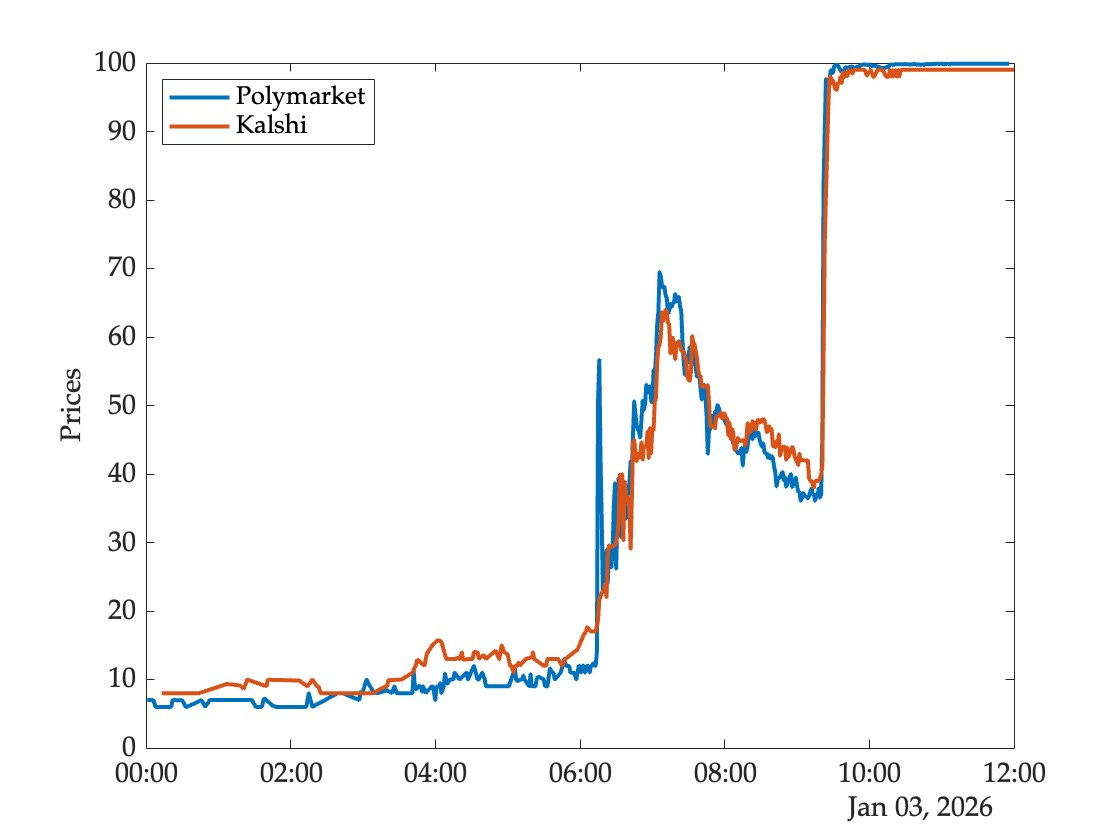

Unlike Polymarket, Kalshi is a regulated exchange that does have to abide by KYC requirements, and prohibits trading by those with inside information. So it’s interesting to compare the price movements on these two exchanges at one minute frequencies over the twelve hour period from midnight to noon UTC on January 3 (7pm January 2 to 7am January 3 on the East Coast):

The trader in question made three large transactions during this window, buying about 260,000 shares at prices in the 7-9 cent range between 1:38am and 2:58am UTC (the other four transactions were made earlier). These trades had very little immediate price impact. In fact, until about 6am UTC prices on Kalshi were higher than those on Polymarket.

Then, at about 6:15am UTC (1:15am on the East Coast) an entirely different trader bought more than 45,000 shares at an average price of 51 cents in a single transaction. You can see this as the price spike (quickly reversed) in the Polymarket chart. Aside from this aberration, prices on the two exchanges track each other closely.

The tight correspondence of prices across exchanges with very different rules and participant populations is a consequence of arbitrage. For example, if the prices of contracts referencing the same event were 20 on one market and 30 on another, a trader could bet on the event at 20 and bet against it at 70, effectively buying a dollar for ninety cents. This is not entirely without risk, since contract rules may be interpreted in different ways by different exchanges, but such occurrences are rare and prices generally move in tandem across markets. That is, insider trading anywhere affects prices everywhere.

In response to this incident, Deva Hazarica dryly observed that “prediction markets have made government work a lot more lucrative.” To this one might add that a very different type of person is now attracted to public service.

Since the price action from anonymous, unregulated exchanges bleeds into everywhere else…

Do you have any policy recommendations? Or does the future consist of govt and corporate information being systematically monetized by insiders? (Not good imo)

And not to say this didn’t happen before in various ways - but this is a more direct, unenforced method unhindered by the SECs public enforcement actions.

Here because you’re on the Oxford reading list. Staying because I’m genuinely interested in this content! Every post teaches me more.

- Another inspired student