The Price Impact of Margin-Linked Shorts

The real money peer-to-peer prediction market PredictIt just made a major announcement: they plan to margin-link short positions. This will lead to an across-the board decline in the prices of many contracts, especially in the two nominee markets. Given that the prices in these markets are already being referenced by the campaigns, this change could well have an impact on the race.

What margin-linking short positions does is to make it substantially cheaper to bet simultaneously against multiple candidates. Instead of a trader's worst-case loss being computed separately for each position, it is computed based on the recognition that only one candidate can eventually win. So a bet against both Bush and Rubio ought to require less cash than a bet against just one of the two, since we know that a loss on one bet implies a win on the other.

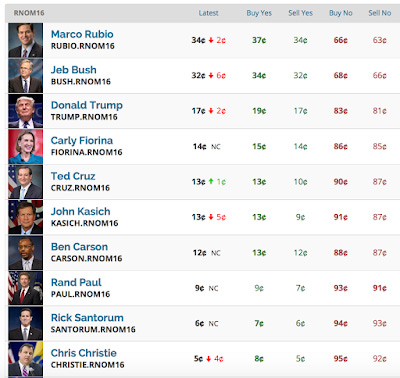

In an earlier post I argued that a failure to margin-link short positions was a design flaw that results in artificially inflated prices for all contracts in a given market, making the interpretation of these prices as probabilities untenable. The problem can be seen by looking at some of the current prices in the GOP nominee market:

The "Buy No" column tells us the price per contract of betting against a candidate for the nomination, with each contract paying out a dollar if the named individual fails to secure the nomination. One could buy five of these contracts (Rubio, Bush, Trump, Fiorina, and Carson) for a total of $3.91, and even of one of these were to win, the payoff from the bet would be $4. If, on the other hand, Cruz or Kasich were to be nominated, the bet would pay $5. There is no risk of loss involved.

Margin-linking shorts recognizes this fact, and would make this basket of five bets collectively cost nothing at all. This would be about as pure an arbitrage opportunity as one is likely to find in real money markets. Aggressive bets would be placed on all contracts simultaneously, with consequent price declines.

A useful effect of this change in design is that manipulating the market becomes much harder. Buying contracts to push up a price would be met by a wall of resistance as long as the sum of all contract prices yields an opportunity for arbitrage. To sustain manipulation would require a trader not only to put a floor on the favored contract, but a ceiling on all others. This has been done before, but would be considerably more costly than under the current market design.

I'd be interested to see which prices are affected most as the transition occurs, and how much prices move in anticipation of the change. But no matter how the aggregate decline is distributed across contracts, this example illustrates one important fact about financial markets in general: prices depend not just on beliefs about the likelihood of future events, but also on detailed features of market design. Too uncritical an acceptance of the efficient markets hypothesis can lead us to overlook this somewhat obvious but quite important point.